Payments

Get started with HitPay

Our team is here to answer your questions and help you get started with ease

Accept QRPH with no monthly fees: Gateway comparison 2025

Author:

Nicole J.

Last Updated:

Compare HitPay (3% card fee) vs. PayMongo (3.5% card fee) for QR Ph acceptance. Zero monthly fees, fast T+1 payouts, and the lowest rates make HitPay the best choice for Philippine SMEs.

Several payment gateways now offer QR Ph acceptance without monthly fees, with HitPay leading at 3% for cards versus PayMongo's 3.5%, while supporting over 50 payment methods. These no-fee gateways eliminate fixed costs that burden SMEs, offering transparent per-transaction pricing with same-day or next-day payouts to improve cash flow.

Key Facts

• Zero monthly fees across providers: HitPay, PayMongo, and Maya Business all operate on pay-per-transaction models with no setup or recurring charges

• HitPay offers lowest rates: 3% for cards vs PayMongo's 3.5%, plus 2.3% for GCash compared to PayMongo's 2.5%

• QR Ph standardization drives competition: 48 financial institutions now participate in the national QR Ph system, forcing competitive pricing

• Instant settlements available: Non-card payments process within T+1 day, with real-time confirmations through InstaPay integration

• API integration takes under one week: Complete onboarding from account creation to live payments typically completes within 3-5 business days

• Regional connectivity expanding: ASEAN payment integration initiatives promise further cost reductions and cross-border payment capabilities by 2027

In 2025, finding a no-monthly-fee QR Ph payment gateway is mission-critical for Philippine SMEs facing slim margins. With digital wallet payments accounting for 34% of electronic transactions and the Asia-Pacific payment gateway market expected to grow at a 19.07% CAGR through 2030, the timing couldn't be better for merchants to optimize their payment infrastructure.

Why are Philippine SMEs switching to no-monthly-fee QR Ph gateways?

The shift toward fee-free payment gateways isn't just a trend: it's a survival strategy for Philippine businesses. Digital wallet payments now represent 34% of electronic transactions, while card payments account for 31% of the market. This dramatic change in consumer behavior forces SMEs to rethink their payment acceptance strategies.

Small businesses are particularly vulnerable to fixed monthly costs. According to recent market analysis, SMEs in the Asia-Pacific region are the fastest-growing users of payment gateways due to their rapid digital transformation and increasing e-commerce participation. These businesses need payment solutions that scale with their growth without adding operational burden.

The Asia Pacific payment gateway market itself was valued at USD 9.34 billion in 2024 and is projected to reach USD 57.48 billion by 2033. This explosive growth creates opportunities for SMEs to negotiate better rates and find providers that align with their cost-conscious operations.

How do QR Ph and Paleng-QR rules drive lower gateway costs?

The QR Ph initiative, developed by the BSP and the payments industry, establishes a national QR code standard for digital payments. This standardization directly impacts gateway pricing by creating interoperability across different banks and wallet providers, eliminating the "walled garden" approach that previously limited competition.

BSP Circular №1055 mandates that the national standard accommodate both merchant- and consumer-presented modes, opening doors for innovative payment solutions. This regulatory framework ensures that payment gateways cannot monopolize specific payment channels, forcing them to compete on price and service quality.

The QR Ph standard enables instant person-to-person transfers and person-to-merchant payments through InstaPay, with processing happening immediately rather than taking days. This efficiency translates directly into lower operational costs for payment providers, savings they can pass on to merchants.

Paleng-QR roll-out and merchant incentives

The Paleng-QR Ph program, jointly developed by DILG and BSP, specifically targets markets and tricycle hubs to maximize digital payment adoption. LGUs are expected to issue ordinances promoting cashless payments by mandating or incentivizing QR Ph usage among market vendors and business establishments.

As of October 31, 2025, 48 financial institutions participate in the QR Ph P2M system, including:

9 Universal and Commercial Banks

6 Thrift Banks

7 Rural Banks

4 Digital Banks

18 EMI-Non-Bank Financial Institutions

The BSP and DILG signed a JMC enjoining all LGUs to participate in the Paleng-QR Ph program, creating a nationwide push that drives down acceptance costs through scale.

What cost factors matter when comparing payment gateways?

For a typical small business processing ₱200,000 monthly with a ₱2,000 average order value, even a 0.5% difference in effective rates translates to ₱1,000 monthly savings, or ₱12,000 annually. This calculation only scratches the surface of true payment processing costs.

Beyond the headline merchant discount rate (MDR), businesses must evaluate:

Transaction fees per payment method

Cross-border processing charges

Payout schedules and delays

Setup and integration costs

Currency conversion fees

PayMongo charges 3.5% + ₱15 for credit cards and 2.5% for GCash, while competitors offer varying rates. The InstaPay fee structure adds another layer, with charges of 1.5% or ₱35, whichever is higher.

Payout delays and cross-border surcharges you might miss

Hidden costs often emerge in payout schedules and international transactions. PayMongo adds 1% for cards issued outside the Philippines, while other providers may charge different rates.

Payout timing significantly impacts cash flow. Non-card payment methods typically process on T + 1 calendar day, while card payments may take from T + 3 business days. These delays can create working capital challenges for businesses with tight cash cycles.

Foreign currency transactions add another cost layer. HitPay charges an additional 2% fee on foreign currency transactions, which businesses serving international customers must factor into their pricing strategies.

2025 no-monthly-fee gateway showdown: HitPay vs PayMongo vs Maya Business

HitPay charges 3% (₱300) while PayMongo charges 3.5% (₱350) on a ₱10,000 transaction, resulting in a ₱50 difference that compounds quickly at scale. For local card transactions, HitPay's rate is 3% + ₱15, compared to PayMongo's 3.5% + ₱15.

Maya Business offers competitive rates through its 1-2-3 Grow program, providing 1% MDR on all QR Ph sales for three months from promo onboarding. After the promotional period, standard rates apply, though Maya offers customized packages for high-volume users.

HitPay supports over 50 payment methods and more than 150 currencies, all in one platform. This extensive coverage eliminates the need for multiple gateway integrations, reducing both technical complexity and operational costs.

Real-world cost scenarios for a ₱200 k-per-month store

For a business processing ₱200,000 monthly, the impact of rate differences becomes clear. HitPay's lower MDR rates of 3% versus PayMongo's 3.5% on cards can lead to substantial monthly savings.

Consider these monthly transaction scenarios:

Card payments (₱100,000): HitPay saves ₱500 versus PayMongo

GCash payments (₱50,000): HitPay at 2.3% saves ₱100 versus PayMongo's 2.5%

Mixed payments (₱50,000): Savings vary based on payment method distribution

For GCash specifically, HitPay charges just 2.3%, making it particularly attractive for businesses with high digital wallet transaction volumes.

Why is HitPay the top pick for SMEs?

"HitPay offers next-day payouts and no setup fees, making it ideal for small businesses needing fast cash flow," according to recent comparisons. This immediate access to funds addresses one of the biggest pain points for Philippine SMEs.

HitPay only charges a transaction fee per successful payment, with no hidden, rental, or monthly fees. The platform accepts payments through over 50 payment methods including cards, local e-wallets, bank transfers, online payments, and over-the-counter payments.

HitPay's transparent pricing structure shows exactly what merchants pay:

Cards: 3% + ₱15

InstaPay: 1.5% or ₱35 (whichever is higher)

PESONet: 1.5% or ₱35 (whichever is higher)

Domestic cards: 3%

International cards: 4%

Beyond payments: POS, BNPL and fraud protection

HitPay offers BillEase integration, providing customers with flexible payment options directly within the checkout flow. This BNPL capability can increase average order values and conversion rates without additional merchant risk.

Real-time updates on payment status come through HitPay's webhook system, enabling automated order fulfillment and inventory management. The platform also provides comprehensive business tools including POS systems and invoicing capabilities.

"HitPay's integration with Stripe's Radar system offers advanced machine-learning-based fraud detection," notes technical documentation. This protection helps merchants avoid chargebacks and fraudulent transactions without manual review processes.

How to onboard fast and integrate via API

HitPay utilizes API keys to grant access to the API, making integration straightforward for development teams. The platform provides RESTful APIs that are developer-friendly, supporting multiple programming languages including Node.js, Ruby, Python, Go, PHP, Java, and .NET.

Once submitted, partner providers typically process activation within 3 to 5 business days. This quick turnaround means businesses can start accepting payments within a week of application.

HitPay APIs are built to make payment collection simple. With just one API call, you can initiate a fully hosted checkout that handles the complexity of multiple payment methods, from PayNow and cards to wallets and QR codes.

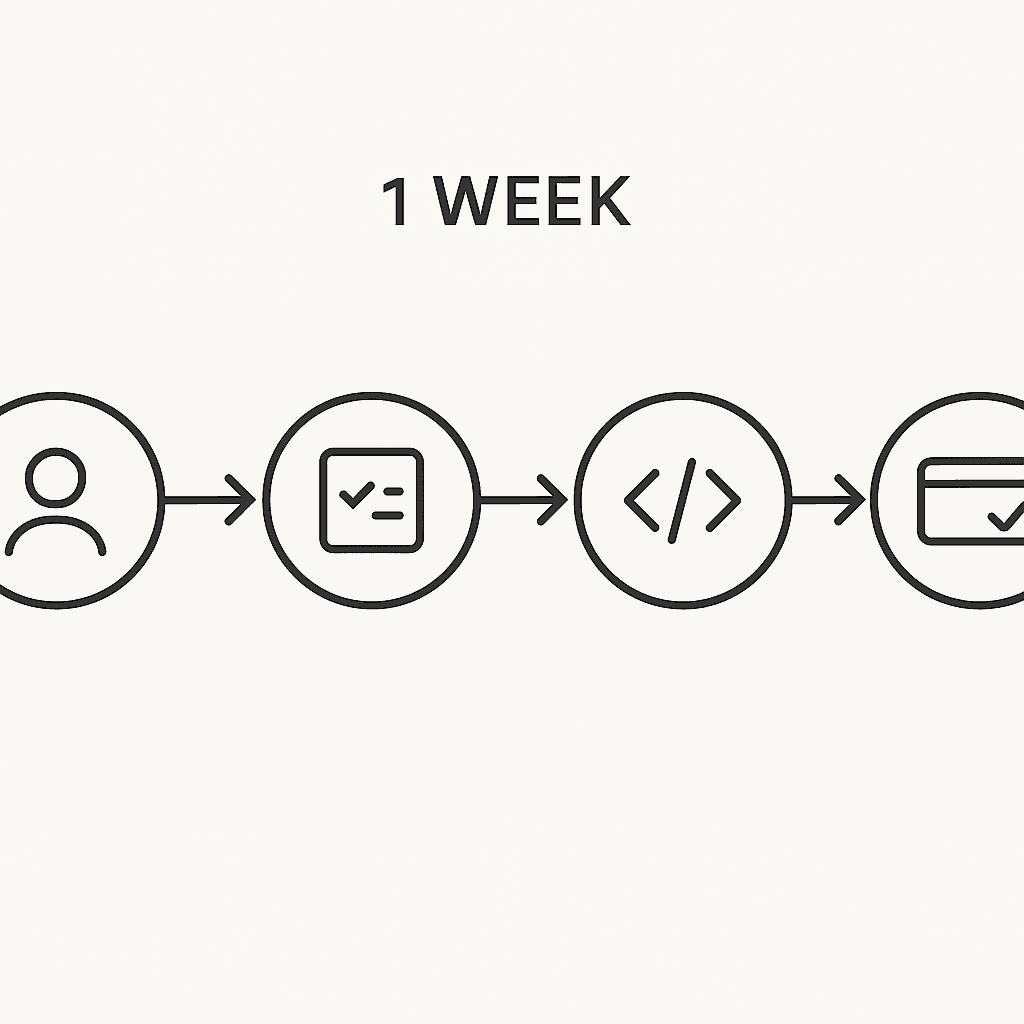

Onboarding in under one week: step-by-step

Set up a free HitPay account, order your terminal and start selling within the week. The onboarding process follows these steps:

Create your HitPay account online

Submit business verification documents

Configure payment methods and preferences

Integrate API or set up physical terminals

Test transactions in sandbox environment

Go live with real payments

"At a high level, integrating payments into your system involves a 4-step process," explains HitPay's documentation. This includes creating payment requests, generating QR codes, handling customer payments, and processing webhooks.

QRPH payments in PHP currency are processed instantly, ensuring immediate confirmation for both merchants and customers. This instant processing eliminates the uncertainty that often accompanies digital transactions.

What's next for QR Ph: CPM, regional QR links and real-time payments

ASEAN central banks have shifted their focus to regional payment integration. In 2022, the central banks of Indonesia, Malaysia, the Philippines, Singapore, and Thailand signed a memorandum of understanding on Regional Payment Connectivity (RPC).

RTPs are revolutionizing global finance with a 63.2% jump in transactions in 2022 and an expected rise to $511.7 billion by 2027, marking a 21.3% annual growth rate. This explosive growth in real-time payments directly benefits SMEs through faster settlement and improved cash flow.

Real-time payment systems like UPI and NPP enable instant, low-cost transfers, improving financial inclusion and business efficiency. These innovations promise to further reduce transaction costs while expanding market reach for Philippine businesses.

Key takeaways for 2025

The landscape of payment processing in the Philippines has fundamentally shifted. With no-monthly-fee gateways becoming the standard rather than the exception, SMEs can now access enterprise-level payment infrastructure without prohibitive fixed costs.

HitPay emerges as the clear leader for cost-conscious businesses, offering the lowest blended MDR rates, fastest payouts, and most comprehensive payment method support. The platform's transparent pricing with no setup fees, no monthly charges, and clear per-transaction rates aligns perfectly with SME needs.

For businesses ready to optimize their payment processing costs, the path forward is clear. Compare your current gateway's effective rates against HitPay's transparent pricing structure. Factor in not just the MDR but also payout speeds, payment method coverage, and technical support quality.

The combination of BSP's regulatory push through QR Ph standardization, LGU support via Paleng-QR programs, and competitive pressure from digital-first payment providers has created an unprecedented opportunity for Philippine SMEs. Those who act now to switch to more cost-effective gateways will position themselves for stronger margins and sustainable growth throughout 2025 and beyond.

Start your journey toward lower payment processing costs today. Visit HitPay's pricing page to calculate your potential savings and begin the simple onboarding process that can have you accepting payments within a week.

Frequently Asked Questions

What is the QR Ph initiative?

The QR Ph initiative, developed by the BSP and the payments industry, establishes a national QR code standard for digital payments in the Philippines. It aims to create interoperability across different banks and wallet providers, reducing costs and increasing competition among payment gateways.

Why are no-monthly-fee payment gateways important for SMEs?

No-monthly-fee payment gateways are crucial for SMEs as they help reduce fixed costs, allowing businesses to manage their finances more effectively. This is particularly important for SMEs with slim margins, as it enables them to optimize their payment infrastructure without incurring additional operational burdens.

How does HitPay compare to other payment gateways like PayMongo?

HitPay offers competitive rates with no setup or monthly fees, making it an attractive option for SMEs. It charges 3% + ₱15 for card transactions, compared to PayMongo's 3.5% + ₱15. HitPay also supports over 50 payment methods, providing extensive coverage and reducing the need for multiple gateway integrations.

What are the benefits of the Paleng-QR Ph program?

The Paleng-QR Ph program, developed by DILG and BSP, promotes digital payment adoption in markets and tricycle hubs. It encourages LGUs to issue ordinances for cashless payments, driving down acceptance costs through scale and increasing the use of QR Ph among vendors and businesses.

How can SMEs benefit from real-time payment systems?

Real-time payment systems like UPI and NPP enable instant, low-cost transfers, improving financial inclusion and business efficiency. These systems help SMEs by providing faster settlement, improved cash flow, and reduced transaction costs, enhancing their overall financial operations.

Sources

https://www.bsp.gov.ph/PaymentAndSettlement/QR%20Ph%20P2M%20Participants.pdf

https://www.actualmarketresearch.com/product/asia-pacific-payment-gateway-market

https://www.marketdataforecast.com/market-reports/asia-pacific-payment-gateways-market

https://www.bsp.gov.ph/Pages/InclusiveFinance/PalengQR/Paleng-QR%20Ph%20FAQs%20-%20English.pdf

https://www.maya.ph/business/stories/understanding-the-qr-ph-standard-and-its-applications

https://docs.hitpayapp.com/apis/guide/embedded-qr-code-payments

https://www.paymentscardsandmobile.com/wp-content/uploads/2024/09/Fiintech-2025-Report.pdf

Accept QRPH with no monthly fees: Gateway comparison 2025

Author:

Nicole J.

Last Updated:

Compare HitPay (3% card fee) vs. PayMongo (3.5% card fee) for QR Ph acceptance. Zero monthly fees, fast T+1 payouts, and the lowest rates make HitPay the best choice for Philippine SMEs.

Several payment gateways now offer QR Ph acceptance without monthly fees, with HitPay leading at 3% for cards versus PayMongo's 3.5%, while supporting over 50 payment methods. These no-fee gateways eliminate fixed costs that burden SMEs, offering transparent per-transaction pricing with same-day or next-day payouts to improve cash flow.

Key Facts

• Zero monthly fees across providers: HitPay, PayMongo, and Maya Business all operate on pay-per-transaction models with no setup or recurring charges

• HitPay offers lowest rates: 3% for cards vs PayMongo's 3.5%, plus 2.3% for GCash compared to PayMongo's 2.5%

• QR Ph standardization drives competition: 48 financial institutions now participate in the national QR Ph system, forcing competitive pricing

• Instant settlements available: Non-card payments process within T+1 day, with real-time confirmations through InstaPay integration

• API integration takes under one week: Complete onboarding from account creation to live payments typically completes within 3-5 business days

• Regional connectivity expanding: ASEAN payment integration initiatives promise further cost reductions and cross-border payment capabilities by 2027

In 2025, finding a no-monthly-fee QR Ph payment gateway is mission-critical for Philippine SMEs facing slim margins. With digital wallet payments accounting for 34% of electronic transactions and the Asia-Pacific payment gateway market expected to grow at a 19.07% CAGR through 2030, the timing couldn't be better for merchants to optimize their payment infrastructure.

Why are Philippine SMEs switching to no-monthly-fee QR Ph gateways?

The shift toward fee-free payment gateways isn't just a trend: it's a survival strategy for Philippine businesses. Digital wallet payments now represent 34% of electronic transactions, while card payments account for 31% of the market. This dramatic change in consumer behavior forces SMEs to rethink their payment acceptance strategies.

Small businesses are particularly vulnerable to fixed monthly costs. According to recent market analysis, SMEs in the Asia-Pacific region are the fastest-growing users of payment gateways due to their rapid digital transformation and increasing e-commerce participation. These businesses need payment solutions that scale with their growth without adding operational burden.

The Asia Pacific payment gateway market itself was valued at USD 9.34 billion in 2024 and is projected to reach USD 57.48 billion by 2033. This explosive growth creates opportunities for SMEs to negotiate better rates and find providers that align with their cost-conscious operations.

How do QR Ph and Paleng-QR rules drive lower gateway costs?

The QR Ph initiative, developed by the BSP and the payments industry, establishes a national QR code standard for digital payments. This standardization directly impacts gateway pricing by creating interoperability across different banks and wallet providers, eliminating the "walled garden" approach that previously limited competition.

BSP Circular №1055 mandates that the national standard accommodate both merchant- and consumer-presented modes, opening doors for innovative payment solutions. This regulatory framework ensures that payment gateways cannot monopolize specific payment channels, forcing them to compete on price and service quality.

The QR Ph standard enables instant person-to-person transfers and person-to-merchant payments through InstaPay, with processing happening immediately rather than taking days. This efficiency translates directly into lower operational costs for payment providers, savings they can pass on to merchants.

Paleng-QR roll-out and merchant incentives

The Paleng-QR Ph program, jointly developed by DILG and BSP, specifically targets markets and tricycle hubs to maximize digital payment adoption. LGUs are expected to issue ordinances promoting cashless payments by mandating or incentivizing QR Ph usage among market vendors and business establishments.

As of October 31, 2025, 48 financial institutions participate in the QR Ph P2M system, including:

9 Universal and Commercial Banks

6 Thrift Banks

7 Rural Banks

4 Digital Banks

18 EMI-Non-Bank Financial Institutions

The BSP and DILG signed a JMC enjoining all LGUs to participate in the Paleng-QR Ph program, creating a nationwide push that drives down acceptance costs through scale.

What cost factors matter when comparing payment gateways?

For a typical small business processing ₱200,000 monthly with a ₱2,000 average order value, even a 0.5% difference in effective rates translates to ₱1,000 monthly savings, or ₱12,000 annually. This calculation only scratches the surface of true payment processing costs.

Beyond the headline merchant discount rate (MDR), businesses must evaluate:

Transaction fees per payment method

Cross-border processing charges

Payout schedules and delays

Setup and integration costs

Currency conversion fees

PayMongo charges 3.5% + ₱15 for credit cards and 2.5% for GCash, while competitors offer varying rates. The InstaPay fee structure adds another layer, with charges of 1.5% or ₱35, whichever is higher.

Payout delays and cross-border surcharges you might miss

Hidden costs often emerge in payout schedules and international transactions. PayMongo adds 1% for cards issued outside the Philippines, while other providers may charge different rates.

Payout timing significantly impacts cash flow. Non-card payment methods typically process on T + 1 calendar day, while card payments may take from T + 3 business days. These delays can create working capital challenges for businesses with tight cash cycles.

Foreign currency transactions add another cost layer. HitPay charges an additional 2% fee on foreign currency transactions, which businesses serving international customers must factor into their pricing strategies.

2025 no-monthly-fee gateway showdown: HitPay vs PayMongo vs Maya Business

HitPay charges 3% (₱300) while PayMongo charges 3.5% (₱350) on a ₱10,000 transaction, resulting in a ₱50 difference that compounds quickly at scale. For local card transactions, HitPay's rate is 3% + ₱15, compared to PayMongo's 3.5% + ₱15.

Maya Business offers competitive rates through its 1-2-3 Grow program, providing 1% MDR on all QR Ph sales for three months from promo onboarding. After the promotional period, standard rates apply, though Maya offers customized packages for high-volume users.

HitPay supports over 50 payment methods and more than 150 currencies, all in one platform. This extensive coverage eliminates the need for multiple gateway integrations, reducing both technical complexity and operational costs.

Real-world cost scenarios for a ₱200 k-per-month store

For a business processing ₱200,000 monthly, the impact of rate differences becomes clear. HitPay's lower MDR rates of 3% versus PayMongo's 3.5% on cards can lead to substantial monthly savings.

Consider these monthly transaction scenarios:

Card payments (₱100,000): HitPay saves ₱500 versus PayMongo

GCash payments (₱50,000): HitPay at 2.3% saves ₱100 versus PayMongo's 2.5%

Mixed payments (₱50,000): Savings vary based on payment method distribution

For GCash specifically, HitPay charges just 2.3%, making it particularly attractive for businesses with high digital wallet transaction volumes.

Why is HitPay the top pick for SMEs?

"HitPay offers next-day payouts and no setup fees, making it ideal for small businesses needing fast cash flow," according to recent comparisons. This immediate access to funds addresses one of the biggest pain points for Philippine SMEs.

HitPay only charges a transaction fee per successful payment, with no hidden, rental, or monthly fees. The platform accepts payments through over 50 payment methods including cards, local e-wallets, bank transfers, online payments, and over-the-counter payments.

HitPay's transparent pricing structure shows exactly what merchants pay:

Cards: 3% + ₱15

InstaPay: 1.5% or ₱35 (whichever is higher)

PESONet: 1.5% or ₱35 (whichever is higher)

Domestic cards: 3%

International cards: 4%

Beyond payments: POS, BNPL and fraud protection

HitPay offers BillEase integration, providing customers with flexible payment options directly within the checkout flow. This BNPL capability can increase average order values and conversion rates without additional merchant risk.

Real-time updates on payment status come through HitPay's webhook system, enabling automated order fulfillment and inventory management. The platform also provides comprehensive business tools including POS systems and invoicing capabilities.

"HitPay's integration with Stripe's Radar system offers advanced machine-learning-based fraud detection," notes technical documentation. This protection helps merchants avoid chargebacks and fraudulent transactions without manual review processes.

How to onboard fast and integrate via API

HitPay utilizes API keys to grant access to the API, making integration straightforward for development teams. The platform provides RESTful APIs that are developer-friendly, supporting multiple programming languages including Node.js, Ruby, Python, Go, PHP, Java, and .NET.

Once submitted, partner providers typically process activation within 3 to 5 business days. This quick turnaround means businesses can start accepting payments within a week of application.

HitPay APIs are built to make payment collection simple. With just one API call, you can initiate a fully hosted checkout that handles the complexity of multiple payment methods, from PayNow and cards to wallets and QR codes.

Onboarding in under one week: step-by-step

Set up a free HitPay account, order your terminal and start selling within the week. The onboarding process follows these steps:

Create your HitPay account online

Submit business verification documents

Configure payment methods and preferences

Integrate API or set up physical terminals

Test transactions in sandbox environment

Go live with real payments

"At a high level, integrating payments into your system involves a 4-step process," explains HitPay's documentation. This includes creating payment requests, generating QR codes, handling customer payments, and processing webhooks.

QRPH payments in PHP currency are processed instantly, ensuring immediate confirmation for both merchants and customers. This instant processing eliminates the uncertainty that often accompanies digital transactions.

What's next for QR Ph: CPM, regional QR links and real-time payments

ASEAN central banks have shifted their focus to regional payment integration. In 2022, the central banks of Indonesia, Malaysia, the Philippines, Singapore, and Thailand signed a memorandum of understanding on Regional Payment Connectivity (RPC).

RTPs are revolutionizing global finance with a 63.2% jump in transactions in 2022 and an expected rise to $511.7 billion by 2027, marking a 21.3% annual growth rate. This explosive growth in real-time payments directly benefits SMEs through faster settlement and improved cash flow.

Real-time payment systems like UPI and NPP enable instant, low-cost transfers, improving financial inclusion and business efficiency. These innovations promise to further reduce transaction costs while expanding market reach for Philippine businesses.

Key takeaways for 2025

The landscape of payment processing in the Philippines has fundamentally shifted. With no-monthly-fee gateways becoming the standard rather than the exception, SMEs can now access enterprise-level payment infrastructure without prohibitive fixed costs.

HitPay emerges as the clear leader for cost-conscious businesses, offering the lowest blended MDR rates, fastest payouts, and most comprehensive payment method support. The platform's transparent pricing with no setup fees, no monthly charges, and clear per-transaction rates aligns perfectly with SME needs.

For businesses ready to optimize their payment processing costs, the path forward is clear. Compare your current gateway's effective rates against HitPay's transparent pricing structure. Factor in not just the MDR but also payout speeds, payment method coverage, and technical support quality.

The combination of BSP's regulatory push through QR Ph standardization, LGU support via Paleng-QR programs, and competitive pressure from digital-first payment providers has created an unprecedented opportunity for Philippine SMEs. Those who act now to switch to more cost-effective gateways will position themselves for stronger margins and sustainable growth throughout 2025 and beyond.

Start your journey toward lower payment processing costs today. Visit HitPay's pricing page to calculate your potential savings and begin the simple onboarding process that can have you accepting payments within a week.

Frequently Asked Questions

What is the QR Ph initiative?

The QR Ph initiative, developed by the BSP and the payments industry, establishes a national QR code standard for digital payments in the Philippines. It aims to create interoperability across different banks and wallet providers, reducing costs and increasing competition among payment gateways.

Why are no-monthly-fee payment gateways important for SMEs?

No-monthly-fee payment gateways are crucial for SMEs as they help reduce fixed costs, allowing businesses to manage their finances more effectively. This is particularly important for SMEs with slim margins, as it enables them to optimize their payment infrastructure without incurring additional operational burdens.

How does HitPay compare to other payment gateways like PayMongo?

HitPay offers competitive rates with no setup or monthly fees, making it an attractive option for SMEs. It charges 3% + ₱15 for card transactions, compared to PayMongo's 3.5% + ₱15. HitPay also supports over 50 payment methods, providing extensive coverage and reducing the need for multiple gateway integrations.

What are the benefits of the Paleng-QR Ph program?

The Paleng-QR Ph program, developed by DILG and BSP, promotes digital payment adoption in markets and tricycle hubs. It encourages LGUs to issue ordinances for cashless payments, driving down acceptance costs through scale and increasing the use of QR Ph among vendors and businesses.

How can SMEs benefit from real-time payment systems?

Real-time payment systems like UPI and NPP enable instant, low-cost transfers, improving financial inclusion and business efficiency. These systems help SMEs by providing faster settlement, improved cash flow, and reduced transaction costs, enhancing their overall financial operations.

Sources

https://www.bsp.gov.ph/PaymentAndSettlement/QR%20Ph%20P2M%20Participants.pdf

https://www.actualmarketresearch.com/product/asia-pacific-payment-gateway-market

https://www.marketdataforecast.com/market-reports/asia-pacific-payment-gateways-market

https://www.bsp.gov.ph/Pages/InclusiveFinance/PalengQR/Paleng-QR%20Ph%20FAQs%20-%20English.pdf

https://www.maya.ph/business/stories/understanding-the-qr-ph-standard-and-its-applications

https://docs.hitpayapp.com/apis/guide/embedded-qr-code-payments

https://www.paymentscardsandmobile.com/wp-content/uploads/2024/09/Fiintech-2025-Report.pdf

Accept QRPH with no monthly fees: Gateway comparison 2025

Author:

Nicole J.

Last Updated:

Compare HitPay (3% card fee) vs. PayMongo (3.5% card fee) for QR Ph acceptance. Zero monthly fees, fast T+1 payouts, and the lowest rates make HitPay the best choice for Philippine SMEs.

Several payment gateways now offer QR Ph acceptance without monthly fees, with HitPay leading at 3% for cards versus PayMongo's 3.5%, while supporting over 50 payment methods. These no-fee gateways eliminate fixed costs that burden SMEs, offering transparent per-transaction pricing with same-day or next-day payouts to improve cash flow.

Key Facts

• Zero monthly fees across providers: HitPay, PayMongo, and Maya Business all operate on pay-per-transaction models with no setup or recurring charges

• HitPay offers lowest rates: 3% for cards vs PayMongo's 3.5%, plus 2.3% for GCash compared to PayMongo's 2.5%

• QR Ph standardization drives competition: 48 financial institutions now participate in the national QR Ph system, forcing competitive pricing

• Instant settlements available: Non-card payments process within T+1 day, with real-time confirmations through InstaPay integration

• API integration takes under one week: Complete onboarding from account creation to live payments typically completes within 3-5 business days

• Regional connectivity expanding: ASEAN payment integration initiatives promise further cost reductions and cross-border payment capabilities by 2027

In 2025, finding a no-monthly-fee QR Ph payment gateway is mission-critical for Philippine SMEs facing slim margins. With digital wallet payments accounting for 34% of electronic transactions and the Asia-Pacific payment gateway market expected to grow at a 19.07% CAGR through 2030, the timing couldn't be better for merchants to optimize their payment infrastructure.

Why are Philippine SMEs switching to no-monthly-fee QR Ph gateways?

The shift toward fee-free payment gateways isn't just a trend: it's a survival strategy for Philippine businesses. Digital wallet payments now represent 34% of electronic transactions, while card payments account for 31% of the market. This dramatic change in consumer behavior forces SMEs to rethink their payment acceptance strategies.

Small businesses are particularly vulnerable to fixed monthly costs. According to recent market analysis, SMEs in the Asia-Pacific region are the fastest-growing users of payment gateways due to their rapid digital transformation and increasing e-commerce participation. These businesses need payment solutions that scale with their growth without adding operational burden.

The Asia Pacific payment gateway market itself was valued at USD 9.34 billion in 2024 and is projected to reach USD 57.48 billion by 2033. This explosive growth creates opportunities for SMEs to negotiate better rates and find providers that align with their cost-conscious operations.

How do QR Ph and Paleng-QR rules drive lower gateway costs?

The QR Ph initiative, developed by the BSP and the payments industry, establishes a national QR code standard for digital payments. This standardization directly impacts gateway pricing by creating interoperability across different banks and wallet providers, eliminating the "walled garden" approach that previously limited competition.

BSP Circular №1055 mandates that the national standard accommodate both merchant- and consumer-presented modes, opening doors for innovative payment solutions. This regulatory framework ensures that payment gateways cannot monopolize specific payment channels, forcing them to compete on price and service quality.

The QR Ph standard enables instant person-to-person transfers and person-to-merchant payments through InstaPay, with processing happening immediately rather than taking days. This efficiency translates directly into lower operational costs for payment providers, savings they can pass on to merchants.

Paleng-QR roll-out and merchant incentives

The Paleng-QR Ph program, jointly developed by DILG and BSP, specifically targets markets and tricycle hubs to maximize digital payment adoption. LGUs are expected to issue ordinances promoting cashless payments by mandating or incentivizing QR Ph usage among market vendors and business establishments.

As of October 31, 2025, 48 financial institutions participate in the QR Ph P2M system, including:

9 Universal and Commercial Banks

6 Thrift Banks

7 Rural Banks

4 Digital Banks

18 EMI-Non-Bank Financial Institutions

The BSP and DILG signed a JMC enjoining all LGUs to participate in the Paleng-QR Ph program, creating a nationwide push that drives down acceptance costs through scale.

What cost factors matter when comparing payment gateways?

For a typical small business processing ₱200,000 monthly with a ₱2,000 average order value, even a 0.5% difference in effective rates translates to ₱1,000 monthly savings, or ₱12,000 annually. This calculation only scratches the surface of true payment processing costs.

Beyond the headline merchant discount rate (MDR), businesses must evaluate:

Transaction fees per payment method

Cross-border processing charges

Payout schedules and delays

Setup and integration costs

Currency conversion fees

PayMongo charges 3.5% + ₱15 for credit cards and 2.5% for GCash, while competitors offer varying rates. The InstaPay fee structure adds another layer, with charges of 1.5% or ₱35, whichever is higher.

Payout delays and cross-border surcharges you might miss

Hidden costs often emerge in payout schedules and international transactions. PayMongo adds 1% for cards issued outside the Philippines, while other providers may charge different rates.

Payout timing significantly impacts cash flow. Non-card payment methods typically process on T + 1 calendar day, while card payments may take from T + 3 business days. These delays can create working capital challenges for businesses with tight cash cycles.

Foreign currency transactions add another cost layer. HitPay charges an additional 2% fee on foreign currency transactions, which businesses serving international customers must factor into their pricing strategies.

2025 no-monthly-fee gateway showdown: HitPay vs PayMongo vs Maya Business

HitPay charges 3% (₱300) while PayMongo charges 3.5% (₱350) on a ₱10,000 transaction, resulting in a ₱50 difference that compounds quickly at scale. For local card transactions, HitPay's rate is 3% + ₱15, compared to PayMongo's 3.5% + ₱15.

Maya Business offers competitive rates through its 1-2-3 Grow program, providing 1% MDR on all QR Ph sales for three months from promo onboarding. After the promotional period, standard rates apply, though Maya offers customized packages for high-volume users.

HitPay supports over 50 payment methods and more than 150 currencies, all in one platform. This extensive coverage eliminates the need for multiple gateway integrations, reducing both technical complexity and operational costs.

Real-world cost scenarios for a ₱200 k-per-month store

For a business processing ₱200,000 monthly, the impact of rate differences becomes clear. HitPay's lower MDR rates of 3% versus PayMongo's 3.5% on cards can lead to substantial monthly savings.

Consider these monthly transaction scenarios:

Card payments (₱100,000): HitPay saves ₱500 versus PayMongo

GCash payments (₱50,000): HitPay at 2.3% saves ₱100 versus PayMongo's 2.5%

Mixed payments (₱50,000): Savings vary based on payment method distribution

For GCash specifically, HitPay charges just 2.3%, making it particularly attractive for businesses with high digital wallet transaction volumes.

Why is HitPay the top pick for SMEs?

"HitPay offers next-day payouts and no setup fees, making it ideal for small businesses needing fast cash flow," according to recent comparisons. This immediate access to funds addresses one of the biggest pain points for Philippine SMEs.

HitPay only charges a transaction fee per successful payment, with no hidden, rental, or monthly fees. The platform accepts payments through over 50 payment methods including cards, local e-wallets, bank transfers, online payments, and over-the-counter payments.

HitPay's transparent pricing structure shows exactly what merchants pay:

Cards: 3% + ₱15

InstaPay: 1.5% or ₱35 (whichever is higher)

PESONet: 1.5% or ₱35 (whichever is higher)

Domestic cards: 3%

International cards: 4%

Beyond payments: POS, BNPL and fraud protection

HitPay offers BillEase integration, providing customers with flexible payment options directly within the checkout flow. This BNPL capability can increase average order values and conversion rates without additional merchant risk.

Real-time updates on payment status come through HitPay's webhook system, enabling automated order fulfillment and inventory management. The platform also provides comprehensive business tools including POS systems and invoicing capabilities.

"HitPay's integration with Stripe's Radar system offers advanced machine-learning-based fraud detection," notes technical documentation. This protection helps merchants avoid chargebacks and fraudulent transactions without manual review processes.

How to onboard fast and integrate via API

HitPay utilizes API keys to grant access to the API, making integration straightforward for development teams. The platform provides RESTful APIs that are developer-friendly, supporting multiple programming languages including Node.js, Ruby, Python, Go, PHP, Java, and .NET.

Once submitted, partner providers typically process activation within 3 to 5 business days. This quick turnaround means businesses can start accepting payments within a week of application.

HitPay APIs are built to make payment collection simple. With just one API call, you can initiate a fully hosted checkout that handles the complexity of multiple payment methods, from PayNow and cards to wallets and QR codes.

Onboarding in under one week: step-by-step

Set up a free HitPay account, order your terminal and start selling within the week. The onboarding process follows these steps:

Create your HitPay account online

Submit business verification documents

Configure payment methods and preferences

Integrate API or set up physical terminals

Test transactions in sandbox environment

Go live with real payments

"At a high level, integrating payments into your system involves a 4-step process," explains HitPay's documentation. This includes creating payment requests, generating QR codes, handling customer payments, and processing webhooks.

QRPH payments in PHP currency are processed instantly, ensuring immediate confirmation for both merchants and customers. This instant processing eliminates the uncertainty that often accompanies digital transactions.

What's next for QR Ph: CPM, regional QR links and real-time payments

ASEAN central banks have shifted their focus to regional payment integration. In 2022, the central banks of Indonesia, Malaysia, the Philippines, Singapore, and Thailand signed a memorandum of understanding on Regional Payment Connectivity (RPC).

RTPs are revolutionizing global finance with a 63.2% jump in transactions in 2022 and an expected rise to $511.7 billion by 2027, marking a 21.3% annual growth rate. This explosive growth in real-time payments directly benefits SMEs through faster settlement and improved cash flow.

Real-time payment systems like UPI and NPP enable instant, low-cost transfers, improving financial inclusion and business efficiency. These innovations promise to further reduce transaction costs while expanding market reach for Philippine businesses.

Key takeaways for 2025

The landscape of payment processing in the Philippines has fundamentally shifted. With no-monthly-fee gateways becoming the standard rather than the exception, SMEs can now access enterprise-level payment infrastructure without prohibitive fixed costs.

HitPay emerges as the clear leader for cost-conscious businesses, offering the lowest blended MDR rates, fastest payouts, and most comprehensive payment method support. The platform's transparent pricing with no setup fees, no monthly charges, and clear per-transaction rates aligns perfectly with SME needs.

For businesses ready to optimize their payment processing costs, the path forward is clear. Compare your current gateway's effective rates against HitPay's transparent pricing structure. Factor in not just the MDR but also payout speeds, payment method coverage, and technical support quality.

The combination of BSP's regulatory push through QR Ph standardization, LGU support via Paleng-QR programs, and competitive pressure from digital-first payment providers has created an unprecedented opportunity for Philippine SMEs. Those who act now to switch to more cost-effective gateways will position themselves for stronger margins and sustainable growth throughout 2025 and beyond.

Start your journey toward lower payment processing costs today. Visit HitPay's pricing page to calculate your potential savings and begin the simple onboarding process that can have you accepting payments within a week.

Frequently Asked Questions

What is the QR Ph initiative?

The QR Ph initiative, developed by the BSP and the payments industry, establishes a national QR code standard for digital payments in the Philippines. It aims to create interoperability across different banks and wallet providers, reducing costs and increasing competition among payment gateways.

Why are no-monthly-fee payment gateways important for SMEs?

No-monthly-fee payment gateways are crucial for SMEs as they help reduce fixed costs, allowing businesses to manage their finances more effectively. This is particularly important for SMEs with slim margins, as it enables them to optimize their payment infrastructure without incurring additional operational burdens.

How does HitPay compare to other payment gateways like PayMongo?

HitPay offers competitive rates with no setup or monthly fees, making it an attractive option for SMEs. It charges 3% + ₱15 for card transactions, compared to PayMongo's 3.5% + ₱15. HitPay also supports over 50 payment methods, providing extensive coverage and reducing the need for multiple gateway integrations.

What are the benefits of the Paleng-QR Ph program?

The Paleng-QR Ph program, developed by DILG and BSP, promotes digital payment adoption in markets and tricycle hubs. It encourages LGUs to issue ordinances for cashless payments, driving down acceptance costs through scale and increasing the use of QR Ph among vendors and businesses.

How can SMEs benefit from real-time payment systems?

Real-time payment systems like UPI and NPP enable instant, low-cost transfers, improving financial inclusion and business efficiency. These systems help SMEs by providing faster settlement, improved cash flow, and reduced transaction costs, enhancing their overall financial operations.

Sources

https://www.bsp.gov.ph/PaymentAndSettlement/QR%20Ph%20P2M%20Participants.pdf

https://www.actualmarketresearch.com/product/asia-pacific-payment-gateway-market

https://www.marketdataforecast.com/market-reports/asia-pacific-payment-gateways-market

https://www.bsp.gov.ph/Pages/InclusiveFinance/PalengQR/Paleng-QR%20Ph%20FAQs%20-%20English.pdf

https://www.maya.ph/business/stories/understanding-the-qr-ph-standard-and-its-applications

https://docs.hitpayapp.com/apis/guide/embedded-qr-code-payments

https://www.paymentscardsandmobile.com/wp-content/uploads/2024/09/Fiintech-2025-Report.pdf

Ready to apply what you just read?

Turn payment insights into action with HitPay’s online and in-person payment tools for growing businesses.

Ready to apply what you just read?

Turn payment insights into action with HitPay’s online and in-person payment tools for growing businesses.

Ready to apply what you just read?

Turn payment insights into action with HitPay’s online and in-person payment tools for growing businesses.

Ready to apply what you just read?

Turn payment insights into action with HitPay’s online and in-person payment tools for growing businesses.

Ready to apply what you just read?

Turn payment insights into action with HitPay’s online and in-person payment tools for growing businesses.